2025 Tax rate & Progressive Tax System explained

Income tax—a tax on money earned from jobs and other sources—is the single largest source of revenue for the United States government. Though controversial when first introduced, income tax has become the foundation of the U.S. tax system, funding public goods such as roads, schools, libraries, and emergency services.

While tax rates change over time, one principle has remained consistent since the 1860s: the United States uses a progressive tax system.

Here’s what that means to you.

Progressive, Regressive, and Flat Taxes Explained

A progressive tax system taxes higher earners at higher rates than lower earners.

For example:

A person earning $10,000 might pay 10% in income taxes

Someone earning $50,000 might pay 20%

Someone earning $100,000 might pay 30%

This simplified example shows how tax rates increase as income rises.

A regressive tax works in the opposite way: lower-income individuals pay a higher percentage of their income than higher-income individuals.

A flat tax applies the same tax rate to everyone, regardless of income. While a flat tax could make filing easier, it may place a heavier burden on lower-income taxpayers and raise fairness concerns.

Why the U.S. Uses a Progressive Tax System

Despite its complexity, a progressive tax system serves several important purposes:

It increases government revenue by collecting more from those who have greater ability to pay, helping fund essential public services.

It reduces the burden on lower-income earners, allowing them greater financial flexibility and opportunity.

It helps address income imbalances, particularly because some types of income—such as dividends and capital gains—are taxed at lower rates than wages.

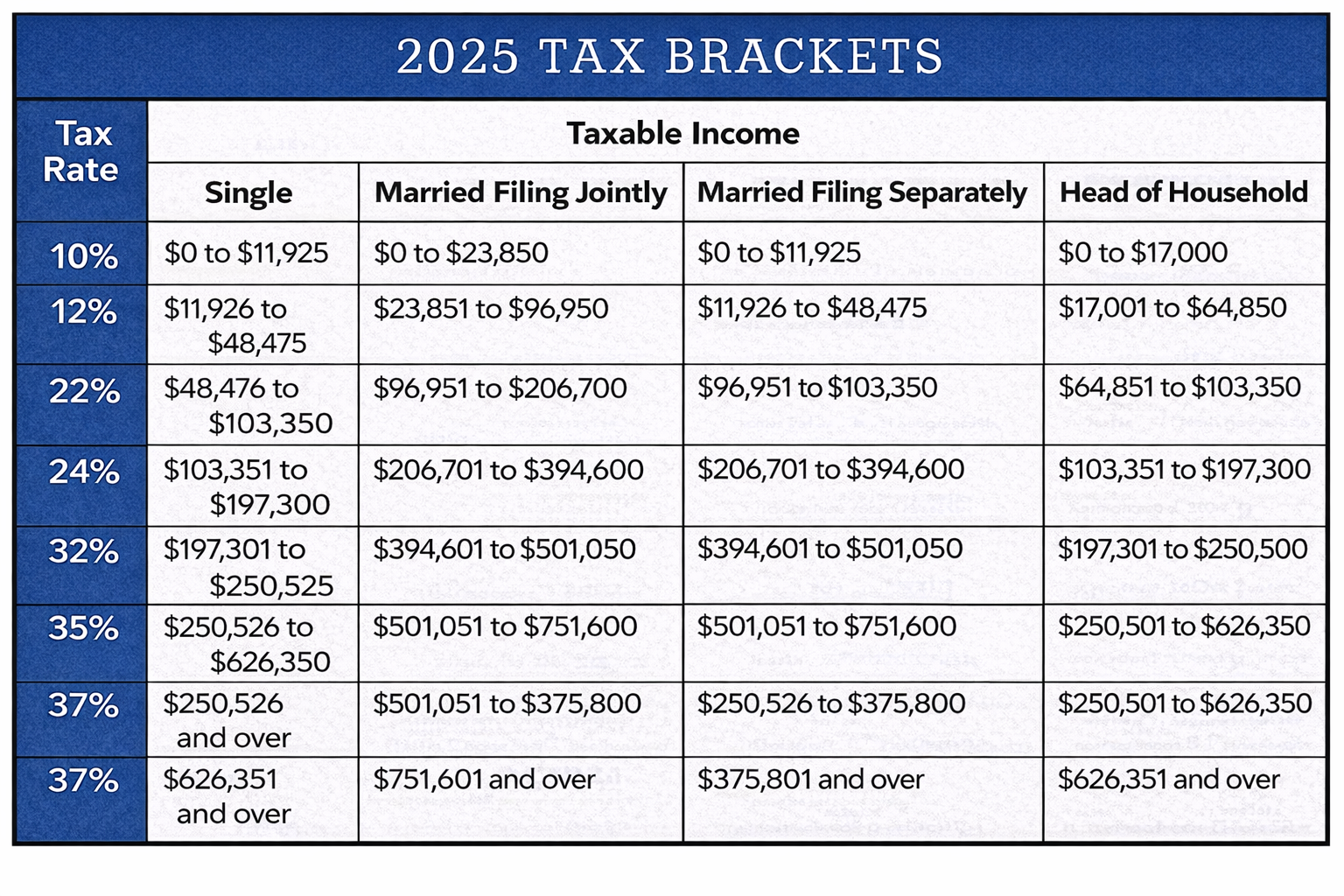

Understanding Tax Brackets

In taxation, progressive has nothing to do with politics. It simply means tax rates increase as income increases.

The federal income tax system currently has seven tax brackets, with rates ranging from 10% to 37%. The income thresholds for each bracket depend on filing status, such as:

Single

Married filing jointly (or qualifying widow/widower)

Married filing separately

Head of household

Not All Income Is Taxed the Same

Your tax bracket is based on your taxable income, not your total income. Taxable income equals total income minus adjustments, deductions, and exemptions.

Taxpayers may choose between:

The standard deduction, a fixed amount set each year, or

Itemized deductions, which can include charitable contributions, education expenses, business costs, mortgage interest, and certain medical expenses.

Deductions can reduce taxable income and, in some cases, move a taxpayer into a lower tax bracket—reducing the total tax owed.

Why This Matters: Marginal Tax Rates

Many people mistakenly believe that earning more income means all of their income is taxed at a higher rate. In reality, only the income within each bracket is taxed at that bracket’s rate.

Understanding Tax Deductions

Tax deductions reduce a taxpayer’s income that is subject to tax, indirectly lowering the total tax owed. The value of a deduction depends on the taxpayer’s marginal tax rate, meaning higher-income taxpayers generally receive a greater benefit from the same deduction. Taxpayers may choose between the standard deduction and itemized deductions, using whichever produces the lowest tax liability.

Standard Deduction

Most taxpayers claim the standard deduction, which is based on filing status and adjusted annually for inflation. The standard deduction simplifies tax filing by allowing a fixed reduction in taxable income without requiring documentation of expenses.

Itemized Deductions

Taxpayers may choose to itemize deductions if the total of eligible expenses exceeds the standard deduction. Itemized deductions include qualifying medical expenses, state and local taxes, mortgage interest, charitable contributions, investment expenses, and certain job-related costs. These deductions require proper documentation and compliance with IRS rules.

The Impact of Deductions and Credits

Deductions and credits affect tax liability in different ways depending on income level and tax bracket. While deductions reduce taxable income, tax credits reduce taxes owed directly. Nonrefundable credits can reduce tax liability only to zero, while refundable credits may generate a refund if tax liability is eliminated.

Tax Brackets and Credit Limitations

Taxpayers in lower tax brackets may not fully benefit from nonrefundable credits if their tax liability is already low or zero. Higher-income taxpayers may receive greater value from deductions due to higher marginal tax rates, highlighting how the same tax benefit can produce different outcomes across income levels.